2022Q2 Quarterly Client Letter

Dear Clients,

Usually, when writing my quarterly newsletter, I focus on only one major topic dominating the market. We’ve looked at the Greek debt crises, Brexit, trade wars, oil prices, the ACA, COVID, and more. This time, we have several things happening at once. We have commodity prices, particularly agricultural and energy, due to the war in Ukraine. We also have a big rotation in the types of stocks that are doing well as lockdowns end and COVID fades (or at least people’s behavioral changes due to COVID) and travel and going out stocks become the market leaders. Then we have rising interest rates, and, finally, we have the biggest worry: a possible recession.

Let’s address the recession risk first. Outside of inflation and the fear that the Fed may raise interest rates too high, there isn’t much reason to think a damaging recession is imminent.

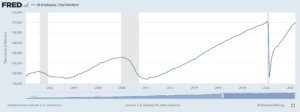

The job market is still strong with a reported 372,000 jobs added last month, and the total number of employed persons (as shown in the graph below) is still climbing and is almost back to its pre-COVID high.

Consumer spending (almost 70% of the economy) is still strong. The graph below shows the total value of all goods and serviced purchased by US consumers (although it’s somewhat affected by inflation).

Furthermore, as of the week that I’m writing this newsletter, large banks and credit card companies are starting to report earnings. So far JP Morgan Chase, Citigroup, Bank of America, Wells Fargo, PNC, US Bancorp, Bank of New York Mellon, and Synchrony have all reported earnings, and across the board have reported healthy consumer credit books and spending levels.

As the Fed raises rates, the other big worry is that it will slow interest rate-sensitive sectors, particularly real estate and the auto sector, as well as increase consumer debt burdens (via higher interest payments). Here again, it’s important to keep in mind that the Fed cut rates down to zero during COVID. It will take both a substantial number of increases for rates to move not only beyond normal levels but also high enough to be considered damaging. Right now, household debt levels (shown below as a percent of GDP) still look fine.

Consumer debt payments (shown below in a chart of household debt service payments compared to disposable income) are still below pre-COVID levels.

Even if we do have a recession, it’s important to remember what that means for your investments. People have been conditioned to think a recession is an end-of-the-world event for investments because of the results of the last two recessions: (1) We had a historically overvalued tech bubble that popped (and technically the recession happened after and probably in part due to the resulting market bubble pop rather than the tech bubble actually being the cause of the market crash) and; (2) in 2008, the greatest consumer debt bubble since the Great Depression popped. None of those conditions are present today, nor are they even close.

Instead, if we do get a recession (and that is not a given) we are likely to get a typical business investment-cycle-led recession. On average, the market is down 25% during a recession, and we’ve already had the market down 25%. In fact, the average 25% drop during a recession isn’t much different than some of the drops we’ve seen with other market panics post 2009.

Ever since 2009, every “crisis” the market has faced has been resolved in a few months and things returned to normal. Now, we are looking at a market that started going down at the beginning of the year. It’s July now, and the market is still down and we may be starting to think, “Hey, what’s going on here?” With recessions it takes on average about a year for the market to recover.

So, what should or can we do?

For clients who have several years to a few decades until retirement, we don’t need to do anything. It’s not a repeat of 2008 or the tech bubble, so there are no long-term concerns.

For clients closer to retirement, especially those only a year or so away, things may be trickier. Ordinarily, bonds, especially Treasury bonds, do well when the market is worried about a recession. Now, however, with inflation high, bonds are also down (although less than stocks). The one bright spot has been Treasury Inflation Protected Bonds (TIPS) whose value goes up when inflation rises. Those have only dropped 8% for the year. For clients taking money out of their portfolio now, we will be drawing from cash, TIPS, and any individual bonds coming due. Also, given that the market on average takes a year to recover, we have been making sure clients close to retirement are keeping some cash available.

Ukraine Donation Challenge Update

I’ve never publicized this by our company gives away approximately 10% of our revenues each year to charitable causes. In our previous newsletter we announced a $10,000 donation challenge to benefit Ukraine. I will match any donations to any charitable organization helping Ukraine up to a $10,000 total. I’m happy to say that we have already matched $5,000 in donations and made our second donation of $2,500, this time to Razom Ukraine.

You can give to a charity of your choice. If you are unsure, below is a list of charities or organization helping Ukraine that I have seen listed in multiple mainstream media publications as reputable (or recommended by Ukrainians).

We will be splitting our matching donations equally amongst: Nova Ukraine (done! – $2500), Red Cross, Save the Children (done! – $2500 donated), and Doctors Without Borders. However, as I said before you can donate to any organization you wish, listed below or not listed, it’s up to you.

Humanitarian – Ukraine based Organizations

Nova Ukraine: https://novaukraine.org/

Razom Ukraine: https://razomforukraine.org/

Sunflowers of Peace: https://www.facebook.com/sunflowerofpeace/

Humanitarian – Global Organizations

International Committee of the Red Cross: https://www.icrc.org/en/where-we-work/europe-central-asia/ukraine

Doctors Without Borders: https://www.doctorswithoutborders.org/what-we-do/countries/ukraine

Save the Children: https://www.savethechildren.org/us/where-we-work/ukraine

Military

Ukraine Ministry of Defense: https://bank.gov.ua/en/news/all/natsionalniy-bank-vidkriv-spetsrahunok-dlya-zboru-koshtiv-na-potrebi-armiyi

Come Back Alive: https://www.comebackalive.in.ua/

2022 Performance to Date

For 2022 all market returns have been negative so far. The US stock market returned almost -20%, Foreign Developed Market stocks were about the same and Emerging Market returned -14.83%.

Bond markets are negative for the year as well, although down less with inflation protected bonds performing the best.

US Stock Market: -19.98%

Foreign Developed Market: -19.26%

Emerging Markets: -14.83%

US Total Bond Market: -10.34%

International Government Bonds: -9.90%

Investment Grade Corporate Bonds: -12.89%

Inflation Protected Bonds: -8.88%

Real Estate: -20.52%

(All the returns listed are those of the ETFs we use.)

Because all client portfolios are individuals your portfolio will contain a combination of most or all the investments listed as well as others, so its performance will be different. Please see your statements for your exact portfolio details.

Reminder

Although you are all familiar with my investment management and retirement planning services, I want to take time in this newsletter to remind you of the other financial services I offer.

These services are available to clients as part of their comprehensive fee. I work with clients to build monthly budgets, help pick the best credit card offer, and give advice on their existing company retirement plans. Almost anything related to finance or money is something I’m available to help you with. I’ve even helped clients with non-financial things, such as picking out a new car. I enjoy helping clients, so please do not hesitate to give me a call. Shoot me an email or text if there is any way I can be of assistance.

How is Ben Invested?

Here is how my personal portfolio (my SEP IRA at FOLIO Institutional) is positioned for 2018.

My investment breakdown is as follows:

- 31% in our Capital Appreciation Folio

- 32% in our Concentrated Stock Folio

- 31% in our Aggressive Growth ETF Portfolio

- 1% in Real Estate (Vanguard Real Estate Index, VNQ)

- 1% in Emerging Market Stocks (Vanguard Emerging Market Index, VWO)

- 1% in Investment Grade Bonds (Vanguard Total Bond Market Index, BND)

- 1% in Inflation Protected Bonds (Barclays iShares TIPS Index, TIP)

- 1% in Municipal Bonds (iShares S&P National AMT-Free Municipal Bond Index, MUB)

- 1% in International Investment Grade Bonds (Vanguard Intermediate Term International Bond Index, BNDX)

As you can see, I have a stock-heavy portfolio. I believe our strategies for investing offer the best opportunity for long-term wealth creation.

Note: I also have an older IRA account opened during grad school. That account is invested in one stock, Philip Morris International (PM).

Sincerely,

Performance Disclosure:

The performance data presented prior to 2011 represents a composite of all discretionary equity investments in accounts that have been open for at least one year. Any accounts open for less than one year are excluded from the composite performance shown. From time to time clients have made special requests that SIM hold securities in their account that are not included in SIMs recommended equity portfolio, so those investments are excluded from the composite results shown. Performance is calculated using a holding period return formula, reflects the deduction of a management fee of 1% of assets per year, and reflects the reinvestment of capital gains and dividends.

Performance data presented for 2011 and after represents the performance of the model portfolio that client accounts are linked too, reflects the deduction of management fees of 1% of assets per year, and reflects the reinvestment of capital gains and dividends.

The S&P 500 and Dow Jones Developed Market Index are used for comparison purposes and may have a significantly different volatility than the portfolios used for the presentation of SIM’s returns. The term “global stocks” refers to the Vanguard Total World Stock ETF (VT).

A copy of our most recent Form ADV Part 2A and Part 2B is available upon request.